Asset Management

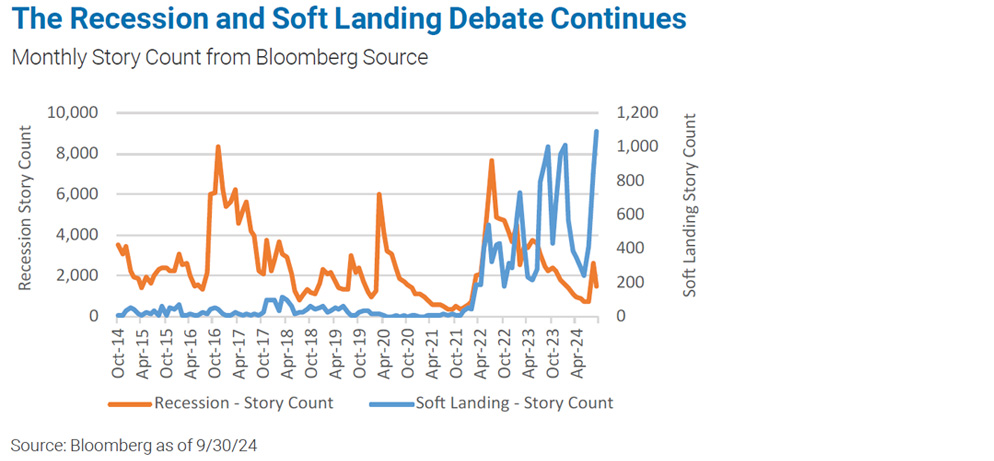

The Landing Debate Continues

October 24, 2024

Economic data remains mixed, with labor markets showing signs of cooling, while consumer spending and corporate earnings remain resilient. Markets are divided, with equities suggesting optimism for a soft landing, while fixed income markets reflect concerns about potential recession risks. We emphasize the need for portfolio diversification, balancing global equities, quality fixed income, and real assets to manage risk and take advantage of opportunities amid ongoing geopolitical and economic uncertainty.

Asset Class Change:

High Yield Credit moved from neutral to slightly negative.

For more information see the asset class detail below.

The lack of a clear trend in the economic data has led to shifting narratives regarding the path forward for markets. Mixed data from the labor market, consumer, corporate fundamentals, and market support OAM Research’s view that proper portfolio diversification going forward is paramount. As the Fed begins its easing cycle, the market is again deliberating the odds of a hard, soft, or no landing.

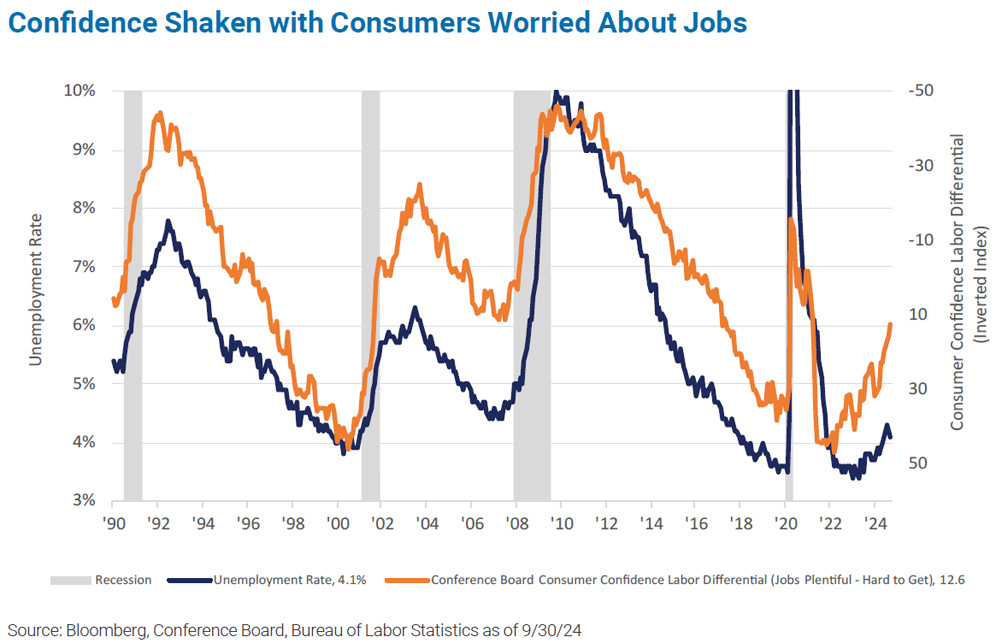

Although the labor market remains healthy, there are signs of some cooling. The unemployment rate, while still low compared to history, has increased by 0.8% from the low of the cycle to 4.1% in September. Payroll growth trends remain uncertain, as the September jobs report was strong but a large negative benchmark revision to the payrolls for the 12 months ending March 2024 erases some earlier resilience. Rising jobless claims and declining consumer confidence also contribute to the mixed outlook. The Fed responded to these risks with a 0.5% rate cut, but the strong September numbers have investors questioning the size of that initial cut.

A major reason a recession has been avoided is the resilience of the U.S. consumer. Despite high inflation, geopolitical risks, restrictive policy, and market volatility, consumer spending has propelled above- trend GDP growth. High levels of employment, strong wage gains, large fiscal stimulus, and asset price appreciation have counteracted weak consumer sentiment readings and enabled consumer spending, particularly in service sectors.

While consumers in aggregate remain healthy, concerning trends are forming in lower income households. While this cohort benefited from the pandemic-era stimulus, excess savings have largely been depleted, forcing lower-income consumers to rely on credit card debt to finance purchases. Delinquencies still remain low but are rising, a factor that likely becomes increasingly problematic if labor softens further.

Despite conflicting signals in labor and consumer data, corporate earnings growth is expected to remain strong, with projections of 10% growth in 2024 and double-digit growth through 2026. Many companies have maintained profitability by passing along price increases to consumers and refinancing debt at low pandemic-era rates, insulating themselves from today’s higher interest rates.

However, concerns remain. Most earnings growth has come from the “Magnificent 7” and as their growth slows, the other 493 companies in the S&P 500 will need to contribute. Additionally, disinflation is reducing corporate pricing power, which had previously supported profit margins.

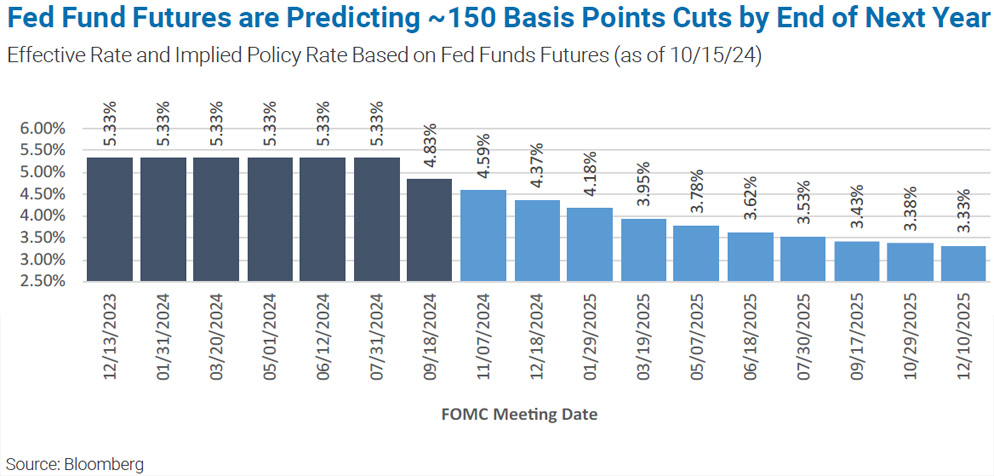

Equities and fixed income offer conflicting views on the U.S. economy. Fixed income markets initially priced in further rate cuts typical of recessions, though expectations eased following the September payrolls report.

In contrast, risk assets suggest confidence in a soft landing, with tight credit spreads and high valuations for large cap stocks, especially in mega-cap growth. However, recent shifts into other sectors may indicate rising skepticism about continued momentum in the “Magnificent 7” and tech-related stocks.

Commodity markets also paint a mixed picture about the global economy. While a rally in gold could indicate a preference for safety, other factors including declining bond yields and rising government debt could be at play as well. Oil price declines over the summer could be indicative of waning global demand, though volatility in recent weeks driven by escalating tensions in the Middle East complicates the macro signal.

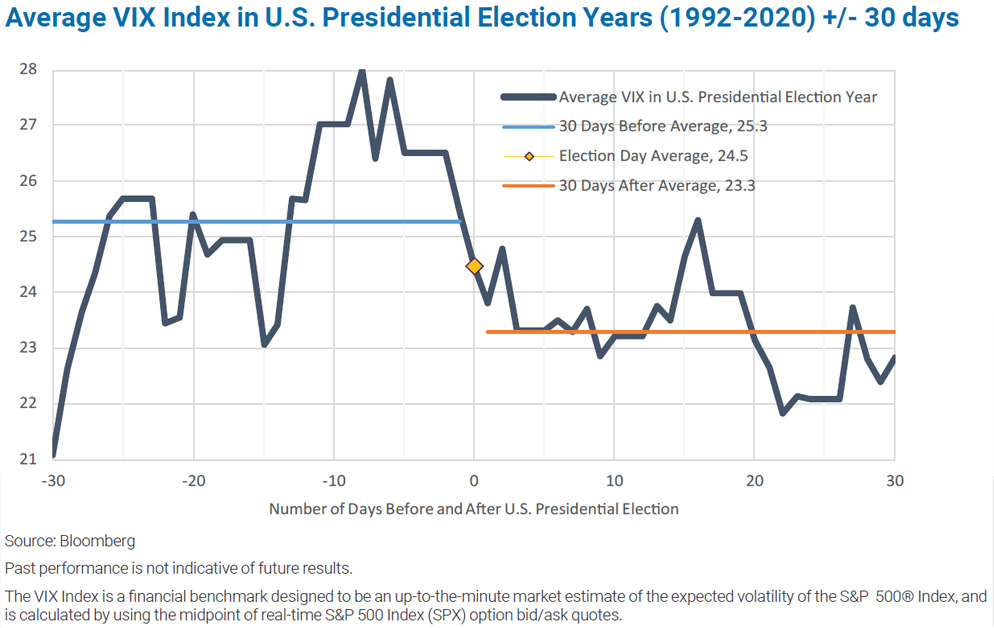

In addition to the uncertainties discussed above, the U.S. election cycle is likely to contribute to market volatility. Historically, there is little evidence of the market favoring one party over another. In a typical presidential election year, equity volatility has risen in the months before November but then falls as investors gain clarity on the makeup of leadership.

Against a backdrop of mixed economic and fundamental data, geopolitical uncertainty, and election-driven volatility, OAM Research continues to stress the need for diversification in portfolios. We remain neutral in our outlook for global equities, reflecting the balance between further upside supported by continued labor market strength and an easing of monetary policy and potential weakness given lofty valuations, particularly in U.S. Large Cap, that suggest too much optimism is priced in. We believe allocating to strategies that emphasize quality has the potential to offer upside participation if the Fed successfully navigates the soft landing and may provide downside protection if the U.S. slips into recession. Investors may also benefit from proper geographical diversification as we believe international developed and emerging market equity valuations remain attractive relative to the U.S.

Fixed income markets appreciated notably in the third quarter, but yields are still attractive and the asset class has the potential to offer diversification benefits in a risk-off environment. We believe core bond allocations stand to appreciate further as the Fed embarks on their cutting cycle, and healthy corporate balance sheets should limit credit risk for higher quality strategies. However, high yield credit spreads are historically tight and could be prone to significant widening if any weakness materializes. Diversifying strategies continue to play an important role in portfolios, particularly as stock-bond correlations remain elevated. In our view, real assets can continue to perform well given their mix of defensive, yield, and diversification characteristics. Merger arbitrage strategies also seek to provide uncorrelated returns and may benefit from renewed M&A activity in a lower rate environment.

Large cap fundamentals remain healthy and earnings growth has been strong. Equity valuations, particularly on the growth side, are stretched compared to history and other asset classes and don’t appear to adequately reflect rising macro headwinds. Higher-quality companies with pricing power should be more resilient, and investors may benefit from allocating to strategies focused on quality and downside protection.

Small and mid-cap stocks no longer trade at discounts after a sharp rebound in July, though valuations remain attractive compared to large caps. Smaller companies are facing the same headwinds as their larger counterparts, primarily due to the impact of higher interest rates, higher cost of labor, and lending pressures but are navigating the environment with less diversified product lines. Smaller cap stocks tend to underperform as economic growth slows, so neutral positioning is warranted.

Economic growth remains tepid but positive in most major economies. Following a weak 2023 and absent a U.S. recession, growth should continue to improve. Earnings growth is expected to trend higher as well. Central banks have made progress on inflation and have begun to cut interest rates, which may provide some relief to more cyclical markets. International equities continue to trade at meaningful discounts compared to U.S. stocks.

Valuations remain reasonable and look attractive relative to developed equities. China’s economy continues to face significant headwinds even after recently announced government stimulus, but other emerging economies have been resilient. Active managers can take advantage of bifurcated performance by allocating to countries with more promising growth prospects.

Long/Short Equity is considered part of the strategic asset allocation for equities based on each fund’s underlying investments.

Long/short strategies seek to benefit from sector rotations and exposure management, as the current environment has been fruitful for shorting. More managers with lower net exposures are exploiting mispricings in the market. The AI trade continues to be present in many hedge fund portfolios, with an overweight to the Magnificent 7 stocks as well as positions in data infrastructure and software application companies.

Yields have moved materially lower as the market priced in an aggressive rate cutting cycle. Still, yields remain relatively attractive, and the asset class should provide portfolio protection in the event of a bumpy landing. Investment-grade credit spreads are still tight, but corporate balance sheets remain healthy. Spreads for high-quality securitized products represent attractive entry points.

Spreads widened in August but then retraced and remain very tight today. The default rate declined in 2024 and remains low relative to history. Absolute yields today remain attractive, but the asset class is priced for perfection and may be subject to a material drawdown if growth stalls.

International bonds have benefited from declining interest rates as global central banks loosen monetary policy. A falling dollar has provided a tailwind that may continue if the Fed cuts rates aggressively. Emerging market debt looks more attractive within the non-U.S. market, both from a yield perspective and as a portfolio diversifier, though the asset class may suffer if global growth slows meaningfully.

Midstream energy infrastructure has remained resilient through a commodity reversal given strong fundamentals and elevated yields. Utilities and Infrastructure stocks can continue to benefit from thematic tailwinds as well as their defensive characteristics. REITs have rebounded strongly on declining interest rates, a tailwind that may persist as the Fed loosens policy.

Event-driven strategies have rebounded from volatility in 2023 and continue to perform well as deals continue to see completion despite heightened regulatory scrutiny and deal flow has begun to recover. Managers with opportunistic credit exposure may additionally benefit from stressed and distressed situations that arise. Other strategies such as multi-manager continue to provide uncorrelated and steady returns with their ability to flexibly lean on multiple sub-strategies amid elevated volatility and higher rates.

Disclosures

The opinions expressed herein are subject to change without notice. The information and statistical data contained herein has been obtained from sources we believe to be reliable. Past performance is not a guarantee of future results.

The above discussion is for illustrative purposes only and mention of any security should not be construed as a recommendation to buy or sell and may not represent all investment managers or mutual funds bought, sold, or recommended for client’s accounts. There is no guarantee that the above-mentioned investments will be held for a client’s account, nor should it be assumed that they were or will be profitable.<

OAM is an indirect, wholly owned subsidiary of Oppenheimer Holdings Inc., which also indirectly wholly owns Oppenheimer & Co. Inc. (Oppenheimer), a registered broker dealer and investment adviser. Securities are offered through Oppenheimer.

For information about the advisory programs available through OAM and Oppenheimer, please contact your Oppenheimer financial advisor for a copy of each firm’s ADV Part 2A.

Adopting a fee-based account program may not be suitable for all investors; anticipated annual commission costs should be compared to anticipated annual fees.

S&P Equal Weighted is the equal-weight version of the S&P 500. The index is comprised of the same stocks of the S&P 500, but each company is allocated a fixed percentage (.2%) of the total index.

MSCI AC World ex-USA Index captures large- and mid- cap representation across 22 of 23 developed-market countries (excluding the U.S.) and 24 emerging-market countries.

MSCI EAFE is an index in U.S. dollars based on the share price of companies listed on stock exchanges in 21 developed countries outside of North America. This Index is created by aggregating the 21 different country Indices, all of which are created separately. It is considered to be generally representative of overseas stock markets.

Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 index. Frank Russell Co. ranks the U.S. common stocks from largest to smallest market capitalization at each annual reconstitution period. The Russell 2000 Index represents a very small percentage of the total market capitalization of the Russell 3000 Index. It is considered to be generally representative of U.S. Equity Small and Mid Cap performance

Russell 1000 Value Index measures the performance of the Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

MSCI Emerging Markets Index is a market capitalization weighted Index in U.S. dollars representing 26 emerging markets in the world. The Index is created by aggregating the 26 different country Indices, all of which are created separately. It is considered to be generally representative of overseas stock markets.

Russell 1000 Growth Index measures the performance of the Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

S&P 500 Sector/Information Technology TR Index consists of stocks chosen for their representation in the Info Tech industry. Companies considered are involved in technology software and technology hardware and equipment. It is a market value weighted Index (stock price times number of shares outstanding), with each stock’s weight in the Index proportionate to its market value.

LTM PE Ratio is the last 12-month price-to-earnings ratio.

Indices are unmanaged, do not reflect the costs associated with buying and selling securities and are not available for direct investment.

Risk Factors

The success of an investment program may be affected by general economic and market conditions, such as interest rates, the availability of credit, inflation rates, economic uncertainty, changes in laws and national and international political circumstances. These factors may affect the level and volatility of securities prices and the liquidity of a portfolio’s investments. Unexpected volatility or illiquidity could result in losses. Investing in securities is speculative and entails risk. There can be no assurance that the investment objectives will be achieved or that an investment strategy will be successful.

Special Risks of Foreign Securities

Investments in foreign securities are affected by risk factors generally not thought to be present in the United States. The factors include, but are not limited to, the following: less public information about issuers of foreign securities and less governmental regulation and supervision over the issuance and trading of securities. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.

Special Risks of Small- and Mid-Capitalization Companies

Investments in companies with smaller market capitalization are generally riskier than investments in larger, well established companies. Smaller companies often are more recently formed than larger companies and may have limited product lines, distribution channels and financial and managerial resources. These companies may not be well known to the investing public, may not have significant institutional ownership and may have cyclical, static or moderate growth prospects. There is often less publicly available information about these companies than there is for larger, more established issuers, making it more difficult for the Investment Manager to analyze that value of the company. The equity securities of small- and mid-capitalization companies are often traded over-the-counter or on regional exchanges and may not be traded in the volume typical for securities that are traded on a national securities exchange. Consequently, the investment manager may be required to sell these securities over a longer period of time (and potentially at less favorable prices) than would be the case for securities of larger companies. In addition, the prices of the securities of small- and mid-capitalization companies may be more volatile than those of larger companies.

Special Risks of Fixed Income Securities

For fixed income securities, there is a risk that the price of these securities will go down as interest rates rise. Another risk of fixed income securities is credit risk, which is the risk that an issuer of a bond will not be able to make principal and interest payments on time. Liquidity risk is the risk that you might not be able to buy or sell investments quickly for a price that is close to the true underlying value of the asset. When a bond is said to be liquid, there’s generally an active market of investors buying and selling that type of bond. Fixed income securities markets are subject to many factors, including economic conditions, government regulations, market sentiment, and local and international political events. Further, the market value of fixed-income securities will fluctuate depending on changes in interest rates, currency values and the creditworthiness of the issuer.

High Yield Fixed Income Risk

High yield fixed income securities are considered to be speculative and involve a substantial risk of default. Adverse changes in economic conditions or developments regarding the issuer are more likely to cause price volatility for issuers of high yield debt than would be the case for issuers of higher-grade debt securities. In addition, the market for high yield debt may be less attractive than that of higher-grade debt securities.

Special Risks of Event-Driven Strategies

Investing in event or disruption driven strategies carries the risk of the unforeseen nature of events, such as corporate transactions falling through or changes in the economic or political environment. A reduction in money market liquidity or pricing inefficiency, as well as other market factors, can potentially reduce the scope for these investment strategies. Such funds may be adversely affected by unforeseen events, including forced redemptions of securities or acquisition proposals, break-up of planned mergers, unexpected changes in relative value, short squeezes, inability to short stock or changes in tax treatment.

Special Risks of Long/Short Equity

Long/short equity strategies utilize leverage, and may do so through direct borrowing, short selling, options and other instruments (including, without limitation, derivatives) and arrangements with embedded leverage. While strategies, techniques and instruments that employ leverage increase the opportunity to achieve higher returns on the amounts invested, they also increase the risk of loss. Hedging and selling securities short entails losing an amount greater than proceeds received or possible default by the other party to the transaction.

Special Risks of Uncorrelated Strategies

Strategies such as multi-strategy, macro and CTA utilize leverage, and may do so through direct borrowing, short selling, options and other instruments (including, without limitation, derivatives) and arrangements with embedded leverage. Hedge funds, commodity pools and other alternative investments involve a high degree of risk and can be illiquid due to restrictions on transfer and lack of a secondary trading market. In addition, they may be subject to commodity risk, derivatives risk, foreign investment risk, foreign currency risk, and credit risk. Many hedge funds employ a single investment strategy. Thus, a hedge fund or even multi-strategy hedge funds may be subject to strategy risk, associated with the failure or deterioration of an entire sub-strategy. Strategy specific losses can result from excessive concentration by multiple hedge fund managers in the same investment or broad events that adversely affect particular strategies.

Special Risks of Alternative Investments

Alternative investments are not appropriate for all investors and only may be offered to certain qualified investors. Investors must be able to bear the economic risk of such an investment for an indefinite period and can afford to suffer the complete loss of investment. An Investor’s ability to redeem from such investments is limited to specific time periods (e.g. monthly, quarterly, semi-annually, annually) with certain notice requirements. Investing in securities is speculative and involves substantial risk. There can be no assurance that any investment strategy will be successful. This information is provided for informational purposes only and should not be construed as an endorsement of or a solicitation to invest in any specific program. There is a substantial risk of loss when investing in alternative investments and, for each specific fund, the risk of underperforming the general markets or other funds.

Special Risks of Real Assets

Master limited partnerships are publicly listed securities that trade much like a stock, but they are taxed as partnerships. MLPs are typically concentrated investments in assets such as oil, timber, gold and real estate. The risks of MLPs include concentration risk, illiquidity, and exposure to potential volatility, tax reporting complexity, fiscal policy and market risk. MLPs are not suitable for all investors. Common risks associated with an investment in a REIT include, but are not limited to, real estate portfolio risk (including development, environmental, competition, occupancy and maintenance risk), general economic risk, market and liquidity risk, interest rate risk, sector diversification and geographic concentration risk, leverage risk, distribution risk, capital markets risk, growth risk, counterparty risk, conflicts of interest risk, key personnel risk, and structural and regulatory risk.

Forward Looking Statements

This presentation may contain forward looking statements or projections. These statements and projections relate to future events or future performance. Forward-looking statements and projections are based on the opinions and estimates of Oppenheimer as of the date of this presentation, and are subject to a variety of risks and uncertainties and other factors, such as economic, political, and public health, that could cause actual events or results to differ materially from those anticipated in the forward-looking statements and projections.

Oppenheimer & Co. Inc. (Oppenheimer), a registered broker/dealer and investment adviser, is a indirect wholly owned subsidiary of Oppenheimer Holdings Inc. Securities are offered through Oppenheimer. If you select one or more of the advisory services offered by Oppenheimer & Co. Inc. (Oppenheimer) or its affiliate Oppenheimer Asset Management Inc. (OAM), the respective entity will be acting in an advisory capacity. Financial planning services are provided by Oppenheimer If you ask us to effect securities transactions for you, Oppenheimer will be acting as a broker-dealer. Please see the Oppenheimer & Co. Inc. website, www.opco.com or call the branch manager of the office that services your account, for further information regarding the difference between brokerage and advisory products and services. Trust services are provided by Oppenheimer Trust Company of Delaware, an affiliate of Oppenheimer. Diversified strategy investments such as natural resources, commodities or futures, real estate investment trusts (REITs), are made available by Oppenheimer only to qualified investors and involve varying degrees of risk. All information provided and opinions expressed are subject to change without notice. Neither Oppenheimer, Oppenheimer Trust Company of Delaware nor OAM provide legal or tax advice. However, your Oppenheimer Financial Professional will work with clients, their attorneys and their tax professionals to help ensure all of their needs are met and properly executed. Investing in securities involves risk and may result in loss of principal. There is no assurance any recommended strategy will be successful. Past performance does not guarantee future results.

© 2024 Oppenheimer & Co. Inc. Transacts Business on All Principal Exchanges and Member SIPC. All rights reserved. No part of this brochure may be reproduced in any manner without the written permission of Oppenheimer. 7203519.1