Asset Management

Instant Insight: Post-Fed Commentary

June 23, 2026

Following each Federal Reserve policy meeting, we provide you with the immediate perspectives of Oppenheimer Asset Management thought leaders. These insights are designed to provide a timely, high- level interpretation of the Fed’s decisions, tone, and implications for the markets. The goal is to equip you with expert-driven, viewpoints in the wake of each FOMC announcement.

With a hold almost fully priced into financial markets, all eyes were on Chair Warsh as he took the podium against a backdrop of sticky inflation, higher oil prices and increasingly hawkish rhetoric from several FOMC participants.

As expected, the Committee voted unanimously (12-0) to leave the federal funds rate unchanged at 3.50% to 3.75%. The most notable development was the dramatically condensed policy statement. At roughly 130 words versus 341 words previously, the statement reflected the new Chair’s apparent preference to reduce the importance of forward guidance, instead concluding with the Federal Reserve’s (Fed's) commitment to “deliver price stability.”

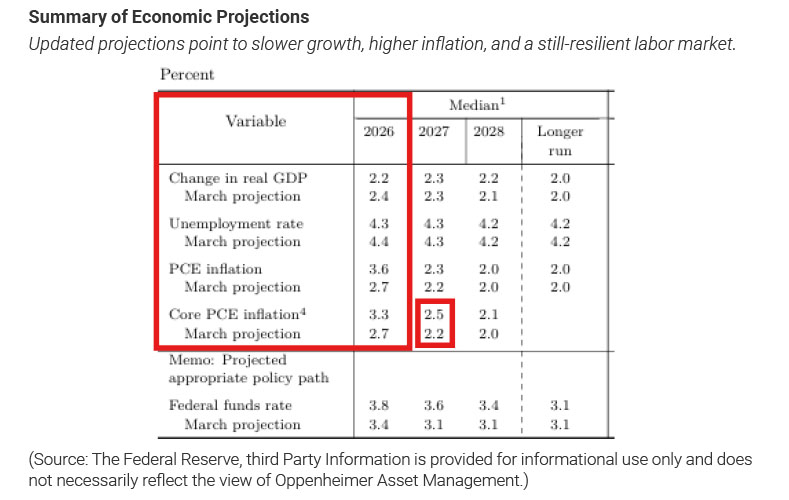

The accompanying Summary of Economic Projections showed a Committee, excluding the Chair’s projections, expecting slightly slower economic growth, a marginally lower unemployment rate and higher inflation in 2026. Taken together, the projections suggest policymakers continue to view the labor market as fundamentally stable despite a less favorable inflation outlook.

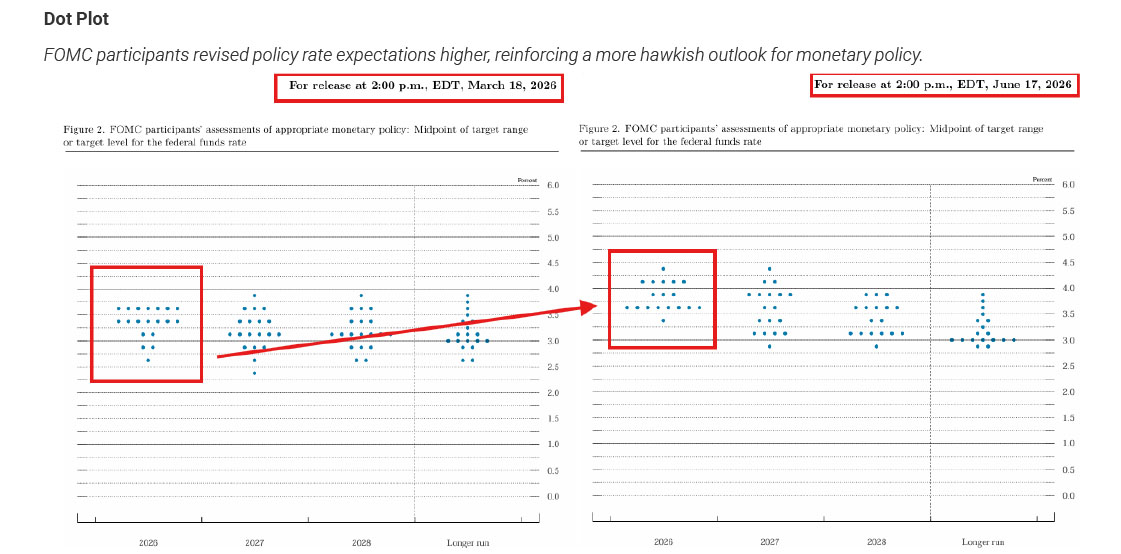

The dot plot also reflected a more hawkish stance from Committee members. Because the Chair’s projections are excluded from the dot plot, it represents only the views of the remaining FOMC participants. The upward shift in projected policy rates raised investor concerns that inflation pressures may extend beyond the recent energy-related price increases.

During the highly anticipated press conference, Chair Warsh clarified several aspects of the Committee’s thinking. While the dual mandate was notably absent from the written statement, the Chair referenced both sides of the mandate, reaffirmed the Fed's commitment to achieving its 2% inflation target and announced the formation of several internal task forces. Most notably, he repeatedly distanced himself from providing any forward guidance, stating that it is “not well suited to current policy at this juncture.”

Although Treasury yields moved sharply higher following the release of the hawkish dot plot, investors should note several comments that were somewhat more balanced than the market reaction implied. Chair Warsh stated that “Fed policy appears to be somewhat restrictive” and added that he would have difficulty making that assessment if financial conditions were not exerting meaningful restraint on economic activity. He also noted that “there was limited discussion about a rate cut today, one proposal was made.” Given the transition to new leadership and the absence of detail regarding which participant advocated for a rate cut, investors are still learning how to interpret the new Committee’s internal dynamics. Overall, the tone of the press conference suggested Committee members (excluding the Chair) that remain highly data dependent, focused on inflation risks and not yet prepared to engage in a discussion of policy easing under the current circumstances.

Newly appointed Fed Chair Warsh kicked off his leadership campaign with a stated goal of limiting the Fed’s forward guidance and communication. The committee presented a unified front with the consensus opting to hold rates steady.

Labor Market – Level: Strong | Trend: Rebounding

Job gains experienced the strongest three-month stretch since early 2024 as the economy added an average of 188,000 per month. The unemployment rate remained at the low level of 4.3%.

Inflation – Level: Elevated | Trend: Cresting (Hopefully)

The Consumer Price Index (CPI) continued to rise in May and hit 4.2% year-over-year, the highest level since April 2023. As positive developments with regard to the Iran conflict have been announced, energy prices have fallen to the lowest levels since the early days of the conflict in March. Investors priced in a much higher probability of a rate hike by year-end after the Fed Chair’s press conference.

The stability of the negotiated peace deal with Iran will go a long way toward making Fed Chair Warsh’s new leadership role a bit easier to manage. Global investors remain hopeful that the end of the conflict is approaching and energy prices will provide an inflationary reprieve.

The Fed’s decision to hold policy rates steady came as little surprise to us given the persistence of inflation alongside continued resilience in economic activity and employment. Recent data suggest that while headline inflation has been pressured higher by energy costs, core inflation remains more contained and is not accelerating. In our view, this combination supports a patient, data-dependent stance from the Committee as it evaluates the path forward under new leadership.

Markets appear to us likely to take the outcome of the meeting in stride, with equities continuing their recent trend to broaden beyond large-cap leadership into mid- and small-cap stocks and a wider range of sectors. We view this rotation as a constructive development, reflecting efforts by investors to reduce overconcentration risk while positioning for opportunities tied to ongoing innovation, particularly in technology and related areas. At the same time, geopolitical dynamics and energy price volatility remain important near-term variables for both inflation and investor sentiment.

In our view, the present environment which is both transitional and potentially transformational reinforces the importance of maintaining perspective amid rapid market responses to incoming news. While short-term volatility is likely to persist, the fundamental backdrop—supported by earnings growth, economic resilience, and innovation—remains intact.

Bottom Line: With inflation still above target but not accelerating broadly, and growth holding firm, the Fed remains on hold for now. We believe investors should stay focused on diversification and long-term fundamentals while navigating a market that continues to adjust to changing conditions.

The views expressed herein reflect current opinions and are not guarantees of future results. Forward looking statements are based on current assumptions and subject to change without notice.

Senior Portfolio Manager OIA Taxable Fixed Income, Oppenheimer Asset Management Inc.

Senior Portfolio Manager OIA Taxable Fixed Income, Oppenheimer Asset Management Inc.

Senior Portfolio Manager OIA Tax-Exempt Fixed Income, Oppenheimer Asset Management Inc.

Head of Research and Investment Management, Oppenheimer Asset Management Inc.

Chief Investment Strategist, Oppenheimer Asset Management Inc.

Oppenheimer & Co. Inc. (Oppenheimer), a registered broker/dealer and investment adviser, is a indirect wholly owned subsidiary of Oppenheimer Holdings Inc. Securities are offered through Oppenheimer. If you select one or more of the advisory services offered by Oppenheimer & Co. Inc. (Oppenheimer) or its affiliate Oppenheimer Asset Management Inc. (OAM), the respective entity will be acting in an advisory capacity. Financial planning services are provided by Oppenheimer If you ask us to effect securities transactions for you, Oppenheimer will be acting as a broker-dealer. Please see the Oppenheimer & Co. Inc. website, www.opco.com or call the branch manager of the office that services your account, for further information regarding the difference between brokerage and advisory products and services. Trust services are provided by Oppenheimer Trust Company of Delaware, an affiliate of Oppenheimer. Diversified strategy investments such as natural resources, commodities or futures, real estate investment trusts (REITs), are made available by Oppenheimer only to qualified investors and involve varying degrees of risk. All information provided and opinions expressed are subject to change without notice. Neither Oppenheimer, Oppenheimer Trust Company of Delaware nor OAM provide legal or tax advice. However, your Oppenheimer Financial Professional will work with clients, their attorneys and their tax professionals to help ensure all of their needs are met and properly executed. Investing in securities involves risk and may result in loss of principal. There is no assurance any recommended strategy will be successful. Past performance does not guarantee future results.

© 2026 Oppenheimer & Co. Inc. Transacts Business on All Principal Exchanges and Member SIPC. All rights reserved. No part of this brochure may be reproduced in any manner without the written permission of Oppenheimer. 8983898.1