Asset Management

The Fed's Evolving Challenge

April 21, 2023

The Fed’s dual mandate of full employment and price stability has effectively morphed into a triple mandate with the additional responsibility of ensuring financial system stability. The collapse of Silicon Valley Bank and its reverberations through the rest of the banking sector have brought questions of financial system stability to the forefront. While price stability remains a key component of the central bank’s mandate, they are now in the unenviable spot of trying to tame higher than target inflation while ensuring the health of the banking system to avoid an economic meltdown.

It may take some time for the impact of the tightening that has already taken place to be fully measured, given the “long and variable” lag between policy action and its economic effect. While the market remains hopeful for a softening stance from the fed, the conflicting growth and inflation data makes forecasting the economic “landing” extremely difficult. We believe the data is unlikely to move in a straight line and the markets will remain unpredictable. Against this backdrop of uncertainty, we continue to believe the potential exists for the economy to experience a slowdown.

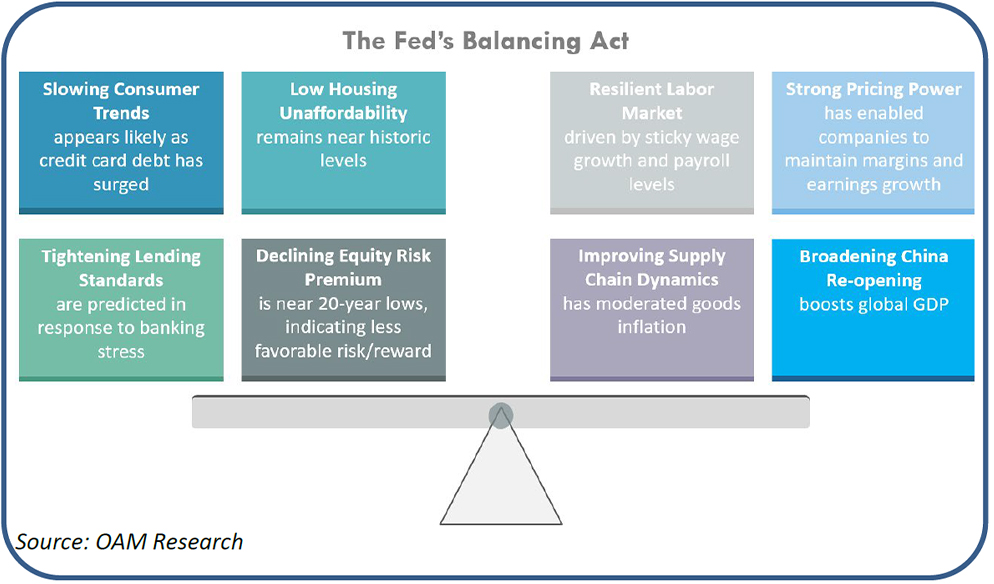

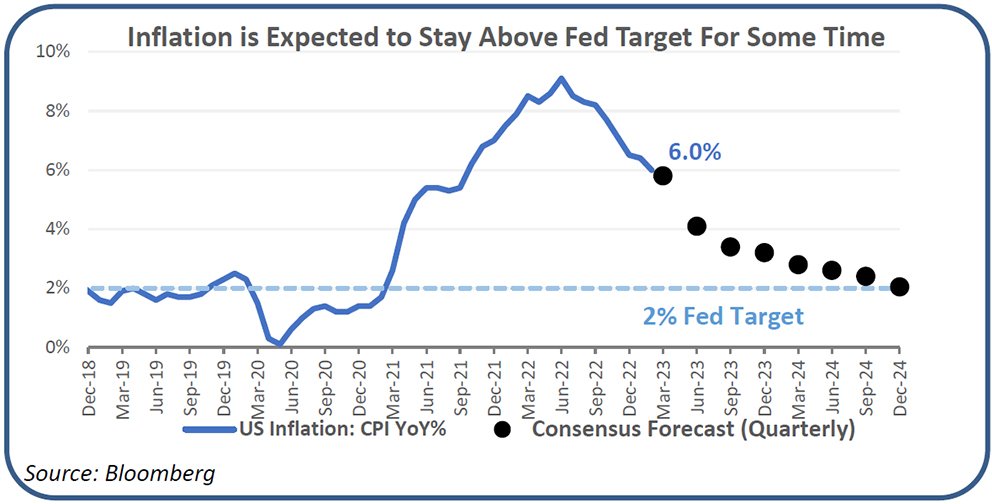

Investors entered 2023 with the expectation that price increases would continue to moderate and the inflation rate would continue its downward trend towards the Fed’s 2% target. The pitfalls of data extrapolation, however, became apparent in February and into March as prices and wage growth remained resilient and sticky. Monthly readings of both headline and core CPI showed that pricing pressures remained for consumers. In addition, both the January and February non-farm payroll numbers far exceeded expectations and displayed strong demand for labor even as layoffs picked up in technology sectors. Wage growth, while tempering month over month, has remained sticky particularly for employees in service industries.

Although the labor market has thus far remained resilient, the effects of tightening monetary policy are beginning to show in other areas of the economy. Notably, higher interest rates have led to housing affordability dropping to all-time lows across many regions, becoming an increasing issue for both sellers and buyers alike. While consumer spending overall has remained fairly strong, and recent retail sales figures have surprised to the upside, U.S. consumers have spent less on discretionary items and relied more on credit as their excess savings from pandemic-related stimulus have been gradually worked down. In addition, while corporate earnings were broadly positive last year, forecasts for 2023 growth have been declining as companies unable to pass through cost increases face margin pressures and slowing demand.

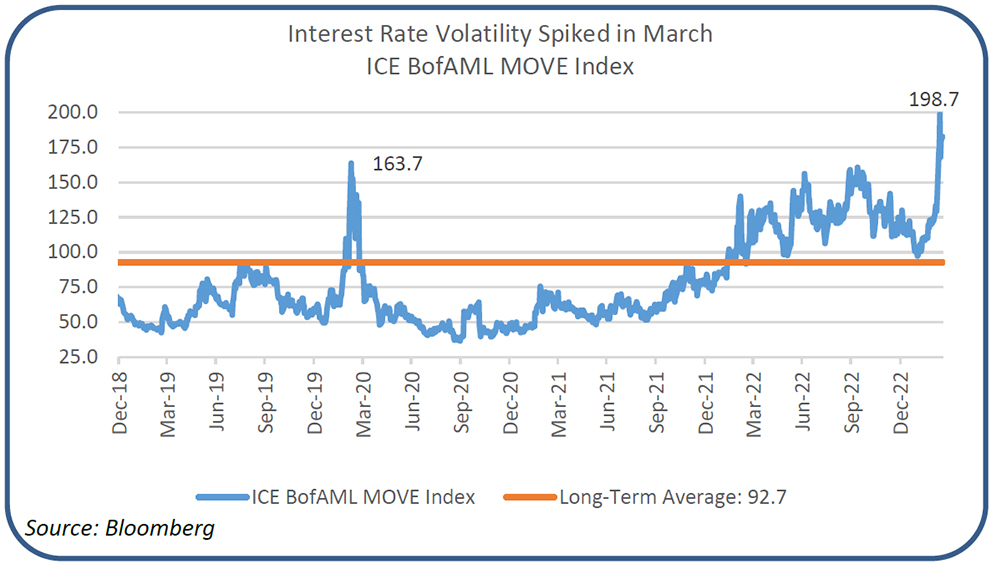

Despite the uncertainty regarding inflation and economic growth, U.S. equities have held up reasonably well year to date. Even with the failures of Silicon Valley Bank and Signature Bank and the resulting fragility of the regional banking sector, U.S. equity volatility (as measured by the CBOE Volatility Index, or “VIX”) is well below levels witnessed in 2022. The same cannot be said for fixed income, however. 2022 saw a notable increase in interest rate volatility (as measured by the ICE BofAML Move Index) against the backdrop of heightened inflation and economic uncertainty. The bank failures announced in March added more volatility to the fixed income markets, spiking the ICE BofAML Move Index to levels surpassing the height of the pandemic.

There is a clear disconnect between recent stock and bond performance and volatility, and the bond market seems to be signaling significant macro headwinds ahead, which may contribute to concerns on a strained consumer and lending capabilities. Notably, we saw no companies with investment grade ratings issue new bonds in mid-March for the first time since 2013 as Treasury market volatility kept companies on the sidelines during a normally busy time for corporate debt financings.

As global central banks make sense of the true impacts of monetary policy tightening that has occurred thus far, OAM Research sees the possibility that inflation remains well above the Fed’s 2% target for some time even as the economy begins to cool, and thus interest rates remain higher than expected and for longer than expected. Against this backdrop, we could see stock-bond correlations remain positive and traditional 60/40 portfolios unable to provide the downside protection investors have grown accustom to. Instead, OAM Research would encourage investors to consider introducing or increasing exposures to truly diversifying strategies such as merger arbitrage with historically lower correlations to traditional asset classes and differentiated return streams.

In the near term, equity markets could potentially see tailwinds from the recent decline in yields, improving supply chains and inventory levels, and the supply / demand benefits of the Chinese economy reopening. However, over the intermediate-term we believe that markets are likely to remain volatile against the uncertain growth and inflation backdrop. Within equity allocations, strategies investing in high quality businesses are expected to be more resilient in a turbulent economic environment. Higher-quality companies with meaningful market share typically have pricing power and can protect their margins during periods of inflation. These companies also tend to have healthier balance sheets and are less reliant on capital markets to fund their businesses, thus they should be minimally impacted by a slowdown in bank lending and are less burdened by higher interest costs.

In fixed income, although yields have compressed recently the asset class still carries its highest yields in over a decade. Interest rate markets are likely to remain volatile as investors sort through central bank actions, but the risk/reward from investment-grade credit looks increasingly attractive, as the asset class should remain protected as defaults and delinquencies rise. With that said, a weaker global economy would serve as a headwind for credit as the pressure on borrowers increases. As such, investors should size their exposure accordingly.

The following Asset Class Detail section summarizes our asset class views.

U.S. Large CapValuations remain extended relative to history and other equities despite the challenging macro backdrop. Higher input costs and slowing consumer demand and spending has led to downward earnings revisions, and more downgrades are likely as persistent inflation leads to further margin pressure. Higher-quality companies with pricing power should be more resilient, and investors may benefit from allocating to strategies focused on quality and downside protection.

Long/Short Equity Long/short strategies should benefit from increased dispersion and market dislocation, leveraging active management of both long and short positions. However, if a broad downward revision of earnings across sectors were to occur, it would likely adversely impact strategies.

Small-cap stocks are trading at a discount compared to history and relative to their large cap counterparts. However, smaller companies are facing the same margin pressure with less diversified product lines. Small caps tend to underperform as economic growth slows, so neutral positioning is warranted despite more attractive valuations.

Although Europe avoided an energy crisis, most major economies are still facing a material economic slowdown and most central banks remain hawkish given the persistence of inflation. International equities continue to trade at meaningful discounts, but given the economic uncertainties there appears to be more downside risk.

Valuations remain reasonable compared to history and look attractive relative to U.S. equities. Still, economic growth in emerging economies is expected to slow meaningfully, and emerging-market stocks tend to be more volatile in the face of uncertainty. Slowing growth and Covid-related lockdowns in China pose a greater risk given the country’s weight in the index and its influence on many other regions.

Interest rates remained very volatile in recent months, first falling precipitously on recession fears and then subsequently rebounding when the Fed reaffirmed its hawkish stance. With a healthy labor market, the Fed is likely to continue raising rates, which will serve as a headwind for core bonds. However, Treasury yields are significantly higher today than they were a year ago, providing a buffer from a total return standpoint.

Rising rates and modest spread-widening have led to higher yields for investment-grade bonds, which are now at 10 year highs. While yields are much more attractive today, the sector still carries significant duration risk and credit spreads could continue to widen as companies face margin pressure.

Spreads are off their recent high of early July but meaningfully wider year to date. The default rate remains below average but defaults have been picking up in 2022 and could accelerate if the economy worsens. But yields for this segment have doubled over this period and high-yield bonds provide higher income today. Investors may prefer short-term high yield that carries a similar yield but with less duration risk.

Yields overseas have improved but remain less attractive than U.S. yields. And investors may face more pain from further central bank tightening and continued U.S. dollar strength. European corporate debt provides less yield than U.S. corporates, and company fundamentals may suffer from a more dramatic economic downturn in Europe. Japan’s rates have stayed low as its central bank tries to remain accommodative in the face of inflation.

Emerging market debt continues to offer attractive absolute yields, but the relative appeal has been reduced as rates rose across most of the developed markets. Although the asset class can be volatile when macro pressures mount, it can provide attractive diversification benefits to portfolios given its low correlation to equities and other fixed income segments.

Midstream energy infrastructure should continue to benefit from elevated oil and gas prices due to constrained supply. Other infrastructure segments with lower equity betas should provide stability in the face of more volatility. REITs have faced pressure from sharp rises in interest rates but may fare better if rates become more range bound.

Macro strategies have performed well in an environment that has seen significant volatility and higher commodity prices. If this environment continues, then we expect their strong performance to continue.

Event-driven strategies continue to perform well as deal flow remains robust and merger processes are relatively insulated from broader volatility. Although M&A activity could slow in the event of a significant slowdown or recession, companies currently continue to widen their competitive moat through acquisitions.

The opinions expressed herein are subject to change without notice. The information and statistical data contained herein has been obtained from sources we believe to be reliable. Past performance is not a guarantee of future results.

The above discussion is for illustrative purposes only and mention of any security should not be construed as a recommendation to buy or sell and may not represent all investment managers or mutual funds bought, sold, or recommended for client’s accounts. There is no guarantee that the above-mentioned investments will be held for a client’s account, nor should it be assumed that they were or will be profitable. OAM Consulting is a division of Oppenheimer Asset Management Inc. (OAM). OAM is an indirect, wholly owned subsidiary of Oppenheimer Holdings Inc., which also indirectly wholly owns Oppenheimer & Co. Inc. (Oppenheimer), a registered broker dealer and investment adviser. Securities are offered through Oppenheimer.

For information about the advisory programs available through OAM and Oppenheimer, please contact your Oppenheimer financial advisor for a copy of each firm’s ADV Part 2A.

Adopting a fee-based account program may not be suitable for all investors; anticipated annual commission costs should be compared to anticipated annual fees.

S&P 500 Index (“SPX”) is a well-known, broad-based stock market unmanaged index which contains only seasoned equity securities. The Fund does not restrict its selection of securities to those comprising the SPX. Performance of the SPX is provided for comparison purposes only. While the Fund’s portfolio may contain some or all of the stocks which comprise the SPX, the Fund does not invest solely in these stocks.

Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000® companies with lower price-to-book ratios and lower expected growth values. The Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics.

Russell 1000 Growth Index measures the performance of the large cap growth segment of the US equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. The Index is constructed to provide a comprehensive and unbiased barometer for the large-cap growth segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect growth characteristics.

NASDAQ Composite Index tracks the performance of about 3,000 stocks traded on the Nasdaq exchange. The index is calculated based on market cap weighting.

VIX Index Created by the Chicago Board Options Exchange (CBOE), the Volatility Index, or VIX, is a real-time market index that represents the market's expectation of 30-day forward-looking volatility. Derived from the price inputs of the S&P 500 index options, it provides a measure of market risk and investors' sentiments.

MSCI AC World ex-USA Index captures large- and mid- cap representation across 22 of 23 developed-market countries (excluding the U.S.) and 24 emerging-market countries.

LTM PE Ratio is the last 12-month price-to-earnings ratio.

Indices are unmanaged, do not reflect the costs associated with buying and selling securities and are not available for direct investment.

Risk Factors

The success of an investment program may be affected by general economic and market conditions, such as interest rates, the availability of credit, inflation rates, economic uncertainty, changes in laws and national and international political circumstances. These factors may affect the level and volatility of securities prices and the liquidity of a portfolio’s investments. Unexpected volatility or illiquidity could result in losses. Investing in securities is speculative and entails risk. There can be no assurance that the investment objectives will be achieved or that an investment strategy will be successful.

Special Risks of Foreign Securities

Investments in foreign securities are affected by risk factors generally not thought to be present in the United States. The factors include, but are not limited to, the following: less public information about issuers of foreign securities and less governmental regulation and supervision over the issuance and trading of securities. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.

Special Risks of Small- and Mid-Capitalization Companies

Investments in companies with smaller market capitalization are generally riskier than investments in larger, well established companies. Smaller companies often are more recently formed than larger companies and may have limited product lines, distribution channels and financial and managerial resources. These companies may not be well known to the investing public, may not have significant institutional ownership and may have cyclical, static or moderate growth prospects. There is often less publicly available information about these companies than there is for larger, more established issuers, making it more difficult for the Investment Manager to analyze that value of the company. The equity securities of small- and mid-capitalization companies are often traded over-the-counter or on regional exchanges and may not be traded in the volume typical for securities that are traded on a national securities exchange. Consequently, the investment manager may be required to sell these securities over a longer period of time (and potentially at less favorable prices) than would be the case for securities of larger companies. In addition, the prices of the securities of small- and mid- capitalization companies may be more volatile than those of larger companies.

Special Risks of Fixed Income Securities

For fixed income securities, there is a risk that the price of these securities will go down as interest rates rise. Another risk of fixed income securities is credit risk, which is the risk that an issuer of a bond will not be able to make principal and interest payments on time. Liquidity risk is the risk that you might not be able to buy or sell investments quickly for a price that is close to the true underlying value of the asset. When a bond is said to be liquid, there's generally an active market of investors buying and selling that type of bond.

Fixed income securities markets are subject to many factors, including economic conditions, government regulations, market sentiment, and local and international political events. Further, the market value of fixed-income securities will fluctuate depending on changes in interest rates, currency values and the creditworthiness of the issuer.

High Yield Fixed Income Risk

High yield fixed income securities are considered to be speculative and involve a substantial risk of default. Adverse changes in economic conditions or developments regarding the issuer are more likely to cause price volatility for issuers of high yield debt than would be the case for issuers of higher grade debt securities. In addition, the market for high yield debt may be less attractive than that of higher-grade debt securities.

Special Risks of Master Limited Partnerships

Master limited partnerships are publicly listed securities that trade much like a stock, but they are taxed as partnerships. MLPs are typically concentrated investments in assets such as oil, timber, gold and real estate. The risks of MLPs include concentration risk, illiquidity, and exposure to potential volatility, tax reporting complexity, fiscal policy and market risk. MLPs are not suitable for all investors.

Forward Looking Statements

This presentation may contain forward looking statements or projections. These statements and projections relate to future events or future performance. Forward-looking statements and projections are based on the opinions and estimates of Oppenheimer as of the date of this presentation, and are subject to a variety of risks and uncertainties and other factors, such as economic, political, and public health, that could cause actual events or results to differ materially from those anticipated in the forward-looking statements and projections. 4870159.1