3/19/2021 Market Commentary

- March 19, 2021

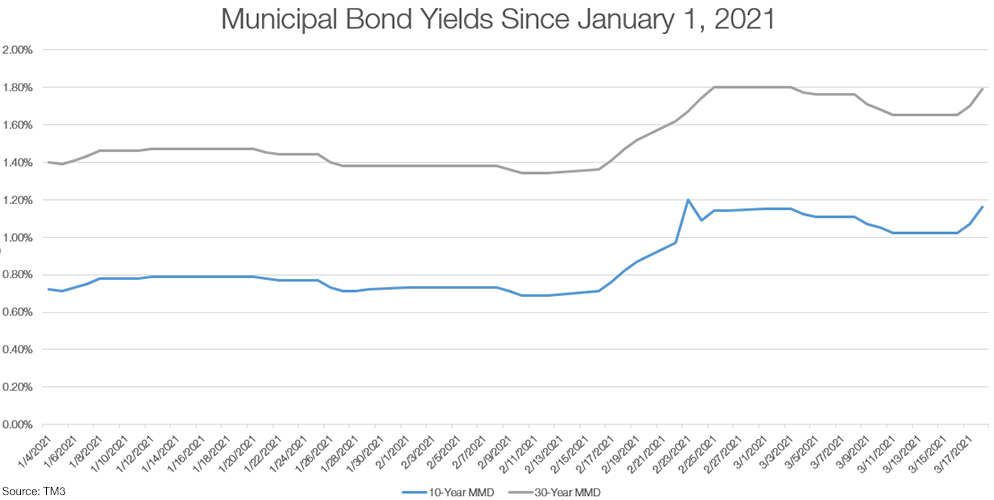

It started off as a quiet week for municipal bonds, with yields holding steady through Tuesday. That changed quickly at the halfway point in the week, with the 10-year and 30-year MMD rising 5 basis points on Wednesday and another 9bps on Thursday.

Tax-exempt yields over the past week:

| 10-Year MMD | 30-Year MMD | |

|---|---|---|

| March 12, 2021 | 1.02% | 1.65% |

| March 18, 2021 | 1.16% | 1.79% |

| Change (bps) | +14 | +14 |

The Federal Reserve’s statement after the Federal Open Market Committee meeting on Wednesday was the primary cause of the jump in rates over the last two days. The Fed voted unanimously to leave the target fed funds rate at near zero, holding on to its stance of keeping rates low until the economy makes a full recovery. Chairmen Powell acknowledged the economic recovery has progressed faster than expected, but stated the recovery has been uneven and incomplete. While the Fed did not waver on their promise to keep rates low, they did increase their projected inflation rate to 2.4% from their earlier 1.8% estimate. The increase in projected inflation was enough to scare Treasury yields, which increased along the curve on Wednesday and Thursday.

Treasury yields over the past week:

| 10-Year Treasury | 30-Year Treasury | |

|---|---|---|

| March 12, 2021 | 1.63% | 2.39% |

| March 18, 2021 | 1.73% | 2.48% |

| Change (bps) | +10 | +9 |

When the Fed’s comments this week caused Treasury yields to rise, Treasury yields pulled tax-exempt yields higher, similar to what we saw happen to the municipal bond market in mid-February. While tax-exempt yields rose sharply this week, it is worth noting that they have still outperformed Treasuries overall since the start of the year. Since January 1st, the 10-year Treasury yield has risen 60 basis points, whereas the 10-year MMD has risen 45 basis points. The difference is even more extreme on the long end, with the 30-year Treasury rising 80 basis points since January 1st, compared to the 30-year MMD only rising by slightly over 40 basis points.

Inflows into municipal bond mutual funds increased to $1.279 billion, beating last week’s mark of $1.092 billion of inflows. As President Biden begins to unveil his plans of increasing the tax rate for higher-earning individuals, demand for tax-exempt municipal bonds is expected to remain strong.

Written by Dan Shaw, Oppenheimer & Co. Inc., Public Finance Associate.

Rick Brandis

Title:Managing Director

Nicki Tallman

Title:Managing Director

Disclaimer

All materials, including proposed terms and conditions, are indicative and for discussion purposes only. Finalized terms and conditions are subject to further discussion and negotiation and will be evidenced by a formal agreement. Opinions expressed are our present opinions only and are subject to change without further notice. The information contained herein is confidential. By accepting this information, the recipient agrees that it will, and it will cause its directors, partners, officers, employees and representatives to use the information only to evaluate its potential interest in the strategies described herein and for no other purpose and will not divulge any such information to any other party. Any reproduction of this information, in whole or in part, is prohibited. Except in so far as required to do so to comply with applicable law or regulation, express or implied, no warranty whatsoever, including but not limited to, warranties as to quality, accuracy, performance, timeliness, continued availability or completeness of any information contained herein is made. Opinions expressed herein are current opinions only as of the date indicated. Any historical price(s) or value(s) are also only as of the date indicated. We are under no obligation to update opinions or other information.

The information contained herein has been prepared solely for informational purposes and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy. Oppenheimer does not provide accounting, tax or legal advice; however, you should be aware that any proposed indicative transaction could have accounting, tax, legal or other implications that should be discussed with your advisors and or counsel. The materials should not be relied upon for the maintenance of your books and records or for any tax, accounting, legal or other purposes. In addition, we mutually agree that, subject to applicable law, you may disclose any and all aspects of any potential transaction or structure described herein that are necessary to support any U.S. federal income tax benefits, without Oppenheimer imposing any limitation of any kind.

Oppenheimer shall have no liability, contingent or otherwise, to the user or to third parties, or any responsibility whatsoever, for the correctness, quality, accuracy, timeliness, pricing, reliability, performance or completeness of the data or formulae provided herein or for any other aspect of the performance of this material. In no event will Oppenheimer be liable for any special, indirect, incidental or consequential damages which may be incurred or experienced on account of the user using the data provided herein or this material, even if Oppenheimer has been advised of the possibility of such damages. Oppenheimer will have no responsibility to inform the user of any difficulties experienced by Oppenheimer or third parties with respect to the use of the material or to take any action in connection therewith. The fact that Oppenheimer has made the materials or any other materials available to you constitutes neither a recommendation that you enter into or maintain a particular transaction or position nor a representation that any transaction is suitable or appropriate for you.

© 2021 Oppenheimer & Co. Inc. Transacts Business on All Principal Exchanges and Member SIPC. All rights reserved. No part of this presentation may be reproduced in any manner without the written permission of Oppenheimer. Oppenheimer & Co. Inc., including any of its affiliates, officers or employees, does not provide legal or tax advice. Investors should consult with their tax advisor regarding the suitability of Municipal Securities in their portfolio.